import pandas as pd회귀 모델에서 계수 p-value의 의미

회귀를 통한 데이터 분석을 수행하면, 계수값과 아울러 계수 값의 p-value도 확인할 수 있습니다.

계수값의 p-value는 어떤 의미를 가지고 있는지 알아보겠습니다.

데이터는 kaggle에 올라와 있는 autompg 데이터셋을 사용했습니다.

df = pd.read_csv('../../autompg-dataset/auto-mpg.csv')df.head()| mpg | cylinders | displacement | horsepower | weight | acceleration | model year | origin | car name | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 18.0 | 8 | 307.0 | 130 | 3504 | 12.0 | 70 | 1 | chevrolet chevelle malibu |

| 1 | 15.0 | 8 | 350.0 | 165 | 3693 | 11.5 | 70 | 1 | buick skylark 320 |

| 2 | 18.0 | 8 | 318.0 | 150 | 3436 | 11.0 | 70 | 1 | plymouth satellite |

| 3 | 16.0 | 8 | 304.0 | 150 | 3433 | 12.0 | 70 | 1 | amc rebel sst |

| 4 | 17.0 | 8 | 302.0 | 140 | 3449 | 10.5 | 70 | 1 | ford torino |

acceleration에 따른 mpg를 회귀 분석 수행한다고 가정하겠습니다.

indep = 'acceleration'

dep = 'mpg'scikit-learn의 LinearRegression을 통해 선형 회귀 분석을 할 수 있습니다.

from sklearn.linear_model import LinearRegressionlr = LinearRegression()# 독립변수 에러로 인해 reshape(-1,1)을 추가하여 주었습니다.

model = lr.fit(df[indep].values.reshape(-1,1), df[dep])# 변수 계수

model.coef_array([1.19120453])# 절편 계수

model.intercept_4.969793004253901선형 회귀를 수행하고, 변수 및 절편의 계수를 확인할 수 있었습니다.

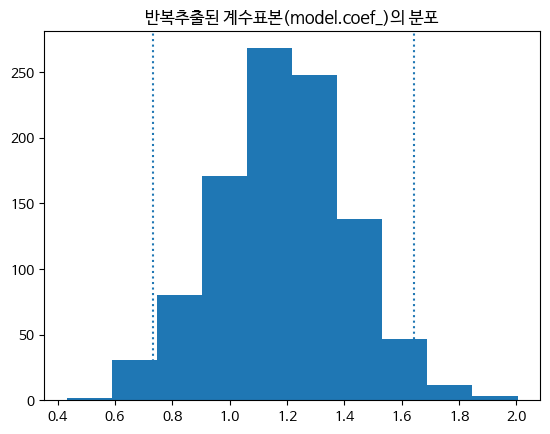

위와 같이 전체에서 선형 회귀를 진행하는 것이 아니라, 일부 샘플을 추출한 다음 선형 회귀식을 만들어 계수를 여러 번 뽑을 수도 있겠습니다.

이를 통해 계수값의 변동성을 아는 것이 목표이자, 동시에 p-value의 기능입니다.

from sklearn.utils import resample반복을 위한 함수를 boot라는 이름으로 정의합니다.

def boot():

idx = resample(range(len(df)), replace=False, n_samples=100)

lr = LinearRegression()

model = lr.fit(df.iloc[idx][indep].values.reshape(-1,1), df.iloc[idx][dep])

return model.coef_[0]values = [boot() for i in range(1000)]import numpy as np# 95% 신뢰구간의 하한

lp = np.quantile(values, q=0.025); lp0.7308445555728666# 95% 신뢰구간의 상한

hp = np.quantile(values, q=0.975); hp1.6430318330598581# 계수의 값

model.coef_array([1.19120453])import matplotlib.pyplot as pltplt.hist(values)

plt.axvline(x=lp, ls=':')

plt.axvline(x=hp, ls=':')

plt.title('반복추출된 계수표본(model.coef_)의 분포')Text(0.5, 1.0, '반복추출된 계수표본(model.coef_)의 분포')

위 결과를 statsmodels로 수행한 p-value 및 신뢰구간과 비교하겠습니다.

import statsmodels.api as smmodel = sm.OLS(df[dep], df[indep])results = model.fit()results.summary()| Dep. Variable: | mpg | R-squared (uncentered): | 0.917 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared (uncentered): | 0.917 |

| Method: | Least Squares | F-statistic: | 4389. |

| Date: | Thu, 19 Jan 2023 | Prob (F-statistic): | 1.02e-216 |

| Time: | 06:02:43 | Log-Likelihood: | -1346.9 |

| No. Observations: | 398 | AIC: | 2696. |

| Df Residuals: | 397 | BIC: | 2700. |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| acceleration | 1.5007 | 0.023 | 66.249 | 0.000 | 1.456 | 1.545 |

| Omnibus: | 11.929 | Durbin-Watson: | 0.760 |

|---|---|---|---|

| Prob(Omnibus): | 0.003 | Jarque-Bera (JB): | 12.496 |

| Skew: | 0.421 | Prob(JB): | 0.00193 |

| Kurtosis: | 2.788 | Cond. No. | 1.00 |

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors assume that the covariance matrix of the errors is correctly specified.

주목해야 할 부분은 coef, P>|t|, 0.025(95% 신뢰구간 하한), 0.975(95% 신뢰구간 상한)입니다.

재표본추출(부트스트랩)을 통해 얻은 결과와 큰 차이가 없음을 알 수 있습니다. 표본통계량의 변동성을 확인할 때는 재표본추출을 사용할 수 있음을 알 수 있습니다.